The difference between a smooth mortgage approval and a stressful declined application often comes down to preparation. Many first home buyers focus exclusively on saving their deposit, only to discover at application time that other factors are holding them back. Whether you are planning to buy in six months or five years, these steps will position you for the strongest possible application when the time comes.

Banks assess mortgage applications based on several key factors: your deposit, your income, your expenses, and your credit history. Each of these areas benefits from advance preparation, and some take considerable time to address if problems exist. Starting early gives you the runway to fix issues rather than discovering them at the worst possible moment.

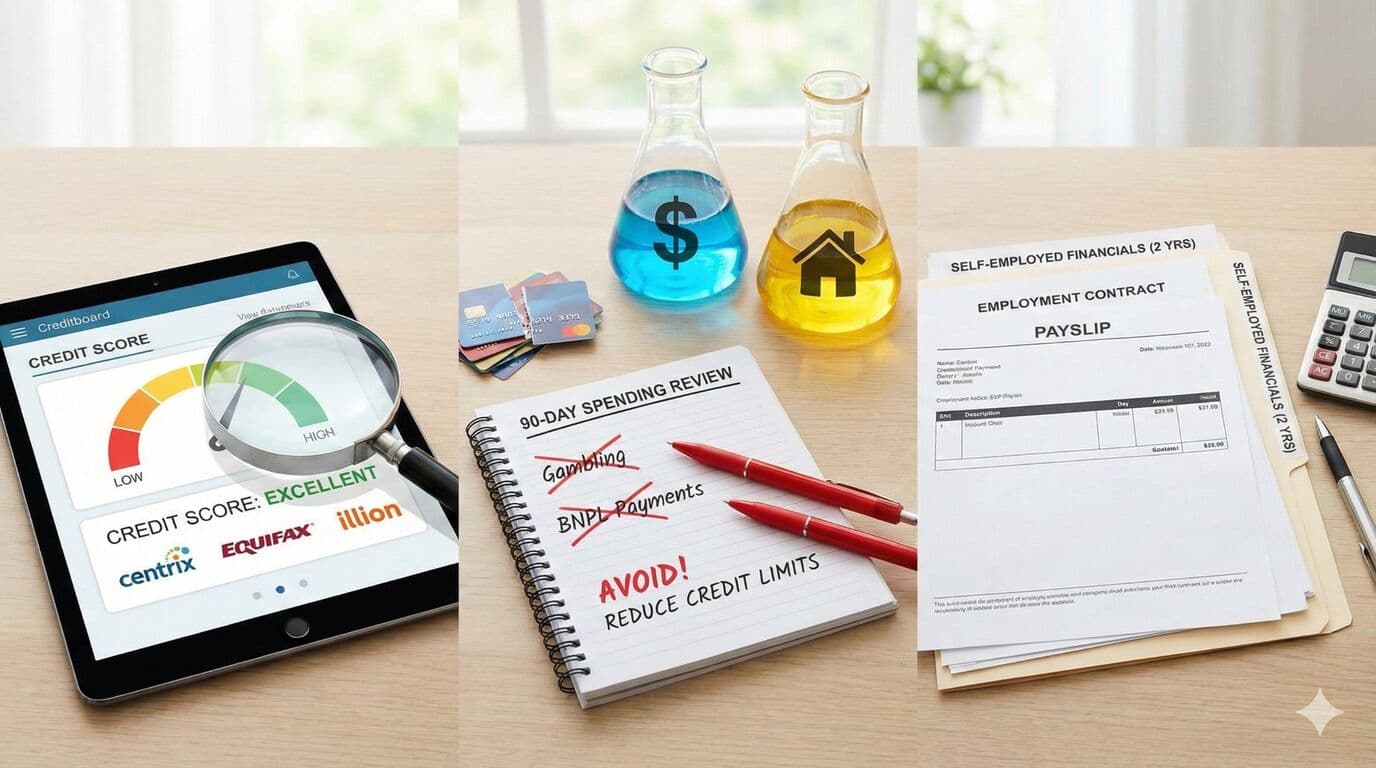

Understanding Your Credit Report

Your credit report is a detailed record of your financial history that lenders use to assess risk. It contains information about every credit account you have held, every payment you have missed, and every time someone has checked your credit. Even small issues on your credit report can raise concerns during mortgage applications.

Most New Zealanders have never looked at their credit report, and many are surprised by what they find. A forgotten overdue phone bill from years ago, a credit card you thought you cancelled, or even someone else's debt incorrectly listed under your name can all appear on your report. These issues do not resolve themselves, and lenders will see them whether you are aware of them or not.

New Zealand has three main credit reporting agencies: Equifax, Centrix, and illion. Each maintains separate records, and lenders may check any or all of them. Obtaining your report from each agency is free and takes only a few minutes online. Equifax offers reports through mycreditfile.co.nz, Centrix through centrix.co.nz, and illion through checkyourcredit.co.nz.

The recommendation is to check your credit report three to four months before applying for a mortgage. This allows time to identify and dispute any errors, settle outstanding debts, or simply understand how your financial history appears to lenders. If you discover significant issues, you may need longer to address them before applying.

Common issues that appear on credit reports include old unpaid utility bills, late payments on buy-now-pay-later services, credit card balances that remain open even when unused, and enquiries from multiple lenders suggesting you have been shopping around desperately for credit. Each of these can be addressed, but the solutions take time.

Maximising Your KiwiSaver Contribution

KiwiSaver represents one of the most powerful tools available to first home buyers in New Zealand. After three years of contributing, most members can withdraw nearly their entire balance to put toward a first home deposit. For someone who has been in KiwiSaver since starting their career, this can represent tens of thousands of dollars.

The standard withdrawal rules allow you to take your entire KiwiSaver balance minus $1,000, which must remain in the account. This includes your own contributions, your employer contributions, and government contributions including the KiwiSaver government contributions. For a typical first home buyer, this withdrawal significantly boosts deposit funds.

To confirm your eligibility and current balance, log into your MyIR account at www.ird.govt.nz. The system will show your total balance and whether you have met the three-year membership requirement. If you are close to three years but not quite there, timing your home purchase to fall after this milestone could add substantially to your deposit.

Increasing your contribution rate now accelerates your KiwiSaver balance growth. If you are currently contributing at the 3.5% default, moving to 4%, 6%, 8%, or even 10% adds directly to your future deposit. Your employer contributes at least 3.5% from 1 April 2026, before ESCT, regardless of your rate, and the government contribution of $260.72 annually is available if you contribute at least $1,042.86 per year and earn under $180,000.

Strengthening Your Income Position

Income directly determines borrowing capacity. Banks calculate how much you can borrow based on your ability to service repayments, and this calculation is highly sensitive to income changes. Even modest income increases can substantially expand your borrowing power.

At current assessment rates around 7.5%, an additional $3,000 in annual income might increase your borrowing capacity by $40,000 to $50,000. For many buyers, this difference determines whether the property they want falls within reach or remains unaffordable.

If a pay rise or promotion is possible, the time to pursue it is before you apply for a mortgage. Banks require evidence of your income, and they want to see stability. A pay increase reflected in two or three pay slips before application carries more weight than a verbal promise of future earnings.

For those with variable income sources, banks typically require six months of consistent history before including that income in their calculations. This includes commission, bonuses, overtime, and self-employment income. If you rely on any of these, ensure you have the documented history to support your application.

Side income and rental income can also boost your borrowing power, but again, documented history matters. Starting a side business three months before your mortgage application will not help, because banks cannot verify its sustainability. However, side income established a year or more ago with consistent earnings can make a meaningful difference.

Reducing Your Expenses and Debt

While income determines how much you can potentially borrow, your expenses and existing debts reduce that figure. Banks assess your uncommitted monthly income, which is what remains after accounting for living costs and debt repayments.

Credit cards deserve particular attention. Banks assess your credit limit, not your actual balance. A $20,000 credit limit card that you never use still counts against your borrowing capacity as if you owed the full amount. Reducing unused credit limits before applying for a mortgage is one of the fastest ways to improve your borrowing position.

Buy-now-pay-later services like Afterpay and Laybuy also affect mortgage applications. Regular use of these services suggests to lenders that you struggle to manage cash flow. Many mortgage advisers recommend avoiding these services entirely in the months leading up to an application.

Car loans, personal loans, and hire purchase agreements all reduce borrowing capacity. If you are considering large purchases before buying a home, understanding how they affect your mortgage position is essential. Sometimes waiting until after settlement for major purchases makes more sense than financing them beforehand.

Your living expenses matter too. Banks will review your bank statements and assess whether your declared expenses match your actual spending. If you claim modest grocery spending but your bank statements show extensive dining out and food delivery, lenders will use the higher actual figure in their calculations.

Living Like a Homeowner

Perhaps the most important preparation is psychological and behavioural. The transition from renting to owning brings financial responsibilities that many buyers underestimate. Practicing homeowner financial habits before you buy builds the discipline that will serve you throughout your mortgage.

Start by budgeting for property-related expenses. Beyond the mortgage payment, homeowners pay rates, insurance, maintenance, and unexpected repairs. Setting aside money each month for these categories helps you understand whether you can genuinely afford home ownership and demonstrates to lenders that you have considered the full picture.

Establish consistent savings patterns. Banks look for evidence that you can save regularly, not just occasionally. Automatic transfers to a dedicated savings account each pay day create the documented history that strengthens applications. The amount matters less than the consistency.

Track your spending carefully for at least three months before applying. Budgeting apps like PocketSmith can help identify where your money actually goes versus where you think it goes. This exercise often reveals opportunities to cut expenses and redirect funds toward your deposit.

Finally, avoid new debt during your preparation period. Every new credit enquiry appears on your credit report, and multiple recent enquiries suggest financial stress. Even if you are approved for new credit, taking on additional debt reduces your mortgage borrowing capacity.

The Advantage of Early Preparation

Mortgage preparation is not something that happens in the weeks before you find a property. The strongest applicants have been preparing for months or even years, building the credit history, savings patterns, and financial discipline that banks want to see.

Starting early also protects you from nasty surprises. Discovering a credit report error when you have three months to fix it is very different from discovering the same error when your purchase is conditional on finance approval. Preparation gives you options that last minute scrambles cannot provide.

Whether you are buying next year or in five years, the habits you build now will serve you throughout your home ownership journey. The mortgage application is just the beginning, and the same discipline that gets you approved will help you manage your property successfully for decades to come.

Need Help With Your Mortgage?

Our expert advisers are here to guide you through every step of your mortgage journey. Get in touch for a free, no-obligation consultation.

Talk to an Adviser