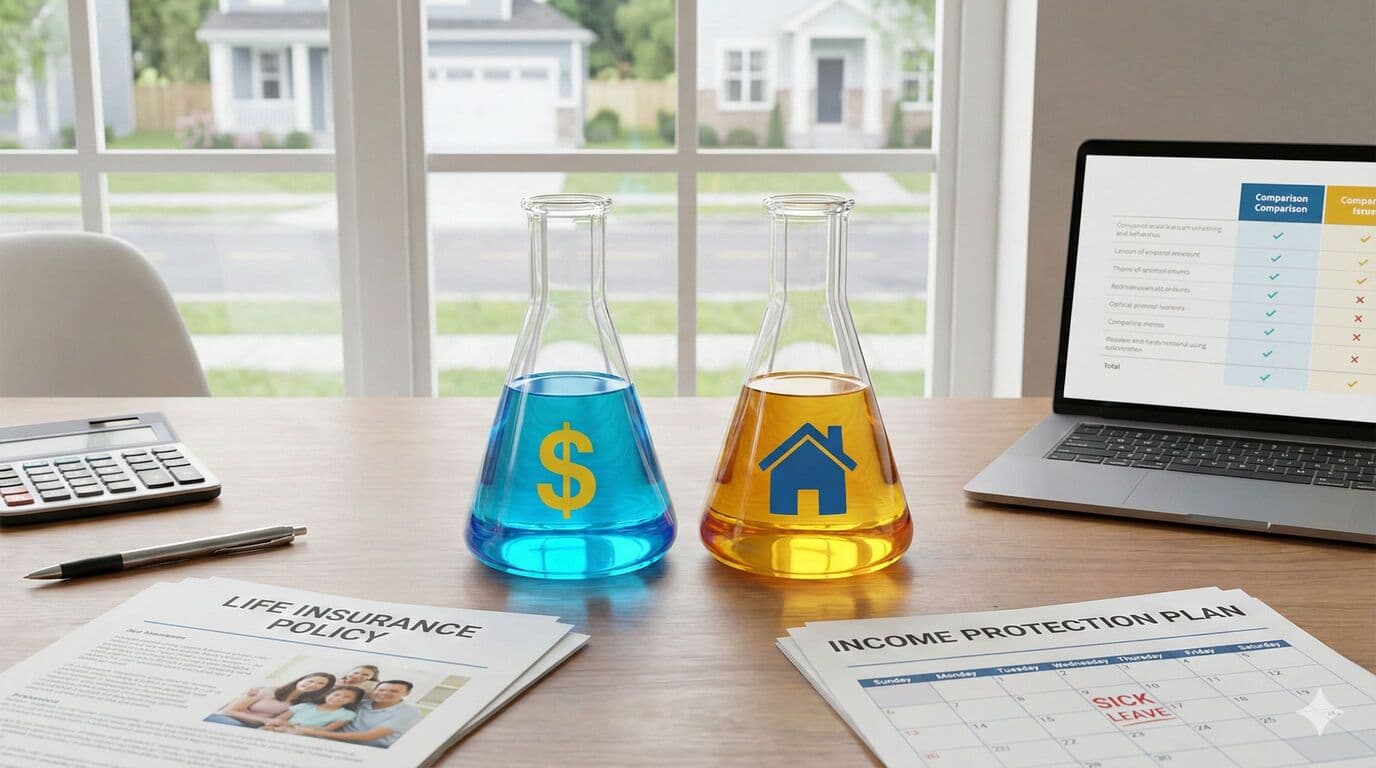

Income protection और life insurance अक्सर confuse होते हैं, लेकिन वे completely different situations cover करते हैं। Life insurance आपके die होने पर pay out करता है। Income protection तब pay out करता है जब आप illness या injury के कारण काम नहीं कर सकते। दोनों को समझना आपको अपने और अपनी family के लिए appropriate protection build करने में help करता है।

आपकी circumstances के depending आपको एक, दोनों, या किसी की भी जरूरत हो सकती है।

Life Insurance Basics

Life insurance आपके die होने पर आपके beneficiaries को lump sum payment provide करता है। यह उन लोगों को protect करता है जो आप पर financially depend करते हैं, वह income और support replace करके जो आप अब provide नहीं कर सकते।

Payout single amount है, ongoing payments नहीं। आपके beneficiaries पूरी sum receive करते हैं जैसे चाहें use करने के लिए: debts pay करना, income के लिए invest करना, या living expenses meet करना।

Life insurance सिर्फ death पर pay out करता है। अगर आप alive हैं लेकिन काम करने में unable हैं तो यह help नहीं करता।

Income Protection Basics

Income protection आपकी income का portion replace करता है अगर आप illness या injury के कारण काम नहीं कर सकते। Life insurance के unlike, आप ही payments receive करते हैं क्योंकि आप अभी भी alive हैं।

Payouts typically आपकी regular income का 75 percent होते हैं, monthly pay होते हैं जब तक आप काम करने में unable रहते हैं, policy limits तक। यह continue होता है जब तक आप काम पर return कर सकते हैं, retirement age reach करते हैं, या आपका policy term end होता है।

Income protection आपको bills pay करने और आपका lifestyle maintain करने में help करता है जब आप ऐसी illness या injury से recover हो रहे हैं जो आपको काम करने से prevent करती है।

आपको दोनों की जरूरत क्यों हो सकती है

एक primary earner वाली family consider करें। अगर वह person die होता है, life insurance lost future income replace करने और debts pay करने के लिए lump sum provide करता है।

अगर वही person seriously ill हो जाता है और दो साल काम नहीं कर सकता, income protection उस period के दौरान bills pay करता रहता है। इसके बिना, family savings burn through कर देती और potentially serious financial difficulty face करती।

ये different risks हैं जिन्हें different solutions की जरूरत है। Death final है; disability temporary या permanent हो सकती है।

कौन सा More Likely है

Statistically, आपकी working life के दौरान significant illness या disability का period होने की ज्यादा likely है बजाय retirement से पहले die होने की। यह income protection को many लोगों के लिए relevant बनाता है।

However, death के consequences typically temporary disability से ज्यादा severe और permanent होते हैं। Life insurance less likely लेकिन more catastrophic outcome address करता है।

दोनों risks real हैं और दोनों आपकी protection planning में consideration deserve करते हैं।

Costs Compare करना

Income protection typically life insurance से more cost करता है equivalent coverage levels के लिए क्योंकि claims more common हैं। Insurers income protection claims पर life insurance claims से ज्यादा frequently pay out करते हैं।

आप जो benefit period और waiting period choose करते हैं वे income protection premiums को significantly affect करते हैं। Shorter waiting periods और longer benefit periods more cost करते हैं।

Life insurance premiums primarily आपकी age, health, और cover amount पर depend करते हैं। Younger, healthier लोग less pay करते हैं।

Waiting Periods Explained

Income protection में payments शुरू होने से पहले waiting period होती है। Common options काम करने में unable होने के बाद 30 days, 60 days, या 90 days हैं।

Waiting period के दौरान, आपको कोई income protection payments नहीं मिलते। इस period को cover करने के लिए आपको other resources जैसे sick leave, savings, या ACC की जरूरत है।

Longer waiting periods premiums significantly reduce करते हैं। अगर आपके पास substantial sick leave entitlements या savings हैं, आप longer waiting period choose कर सकते हैं और less pay कर सकते हैं।

Benefit Periods

Income protection benefit periods determine करते हैं कि payments कितने समय continue होते हैं। Options typically two years से age 65 तक range करते हैं।

Shorter benefit periods temporary conditions के लिए suit करते हैं जिनसे आप recover होने की expect करते हैं। Longer benefit periods permanent disability से protect करते हैं जो आपको फिर कभी काम करने से prevent कर सकती है।

Longer benefit periods more cost करते हैं लेकिन more comprehensive protection provide करते हैं।

अपना Decision लेना

अपनी personal circumstances consider करें। क्या आपके dependents हैं? आपकी family आपकी income के बिना कितने समय manage कर सकती है? अगर आप काम नहीं कर सकते तो आपके पास क्या resources हैं?

Many लोग पहले life insurance prioritise करते हैं क्योंकि death के consequences severe हैं। Income protection disability के more likely risk के against protection की another layer add करता है।

एक financial adviser आपको options समझने और आपकी situation के लिए appropriate protection build करने में help कर सकता है।

Need Help With Your Insurance?

Our expert advisers will help you find the best adviser for you. Get in touch to be connected with a professional insurance adviser.

Talk to an Adviser