Here's a simple mindset shift that can save you tens of thousands of dollars and years off your mortgage: pretend your interest rate is 8%, even when it's not.

This isn't about fear-it's about preparation. When rates are low, you have an opportunity. When they rise, you're already ready.

The Payment Shock Problem

Many homeowners budget their lifestyle around their current mortgage payment. When rates rise, they're caught off guard.

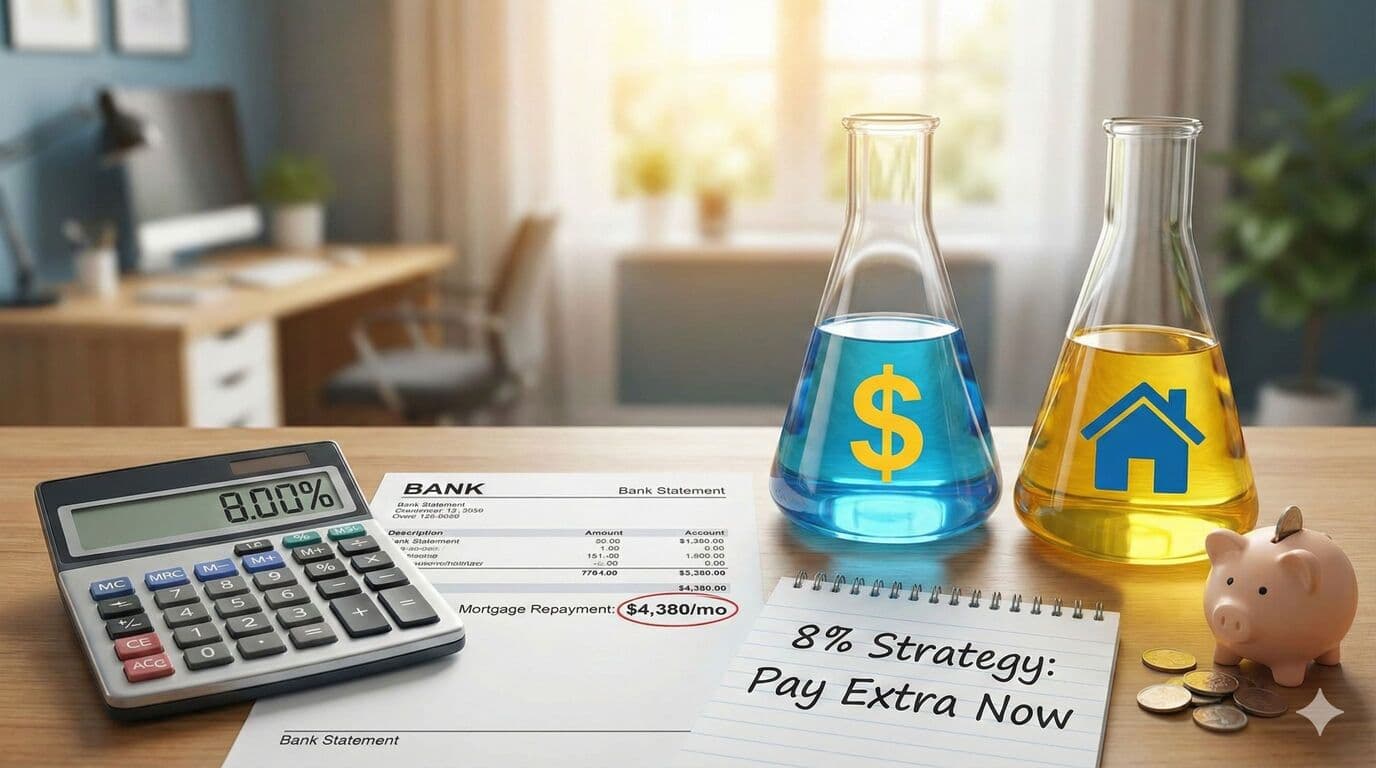

Example: $600,000 mortgage over 30 years

| Interest Rate | Weekly Payment | Monthly Payment |

|---|---|---|

| 5.0% | $740 | $3,210 |

| 6.0% | $825 | $3,575 |

| 7.0% | $915 | $3,970 |

| 8.0% | $1,010 | $4,380 |

That's a $270/week ($1,170/month) difference between 5% and 8%. Could your budget absorb that increase overnight?

The 8% Strategy

The idea is simple: calculate what your repayments would be at 8% interest, then pay that amount now-even though your actual rate is lower.

This approach delivers multiple benefits. First, there's no payment shock when rates rise because you've already adjusted your budget. Second, you'll see massive interest savings since extra payments go straight to principal. Third, overpaying accelerates your payoff date, potentially knocking years off your mortgage. Finally, you gain financial peace of mind knowing you're prepared for whatever happens in the rate environment.

The Numbers: A Worked Example

Let's say you have a $550,000 mortgage at 6% over 30 years.

Current required payment: $760/week

Payment at 8%: $925/week

Difference: $165/week extra

What that $165/week achieves:

| Metric | At Minimum Payment | Paying as if 8% |

|---|---|---|

| Time to pay off | 30 years | 18 years |

| Total interest | $636,000 | $316,000 |

| Interest saved | - | $320,000 |

| Years saved | - | 12 years |

By paying as if your rate were 8%, you'd save $320,000 in interest and be mortgage-free 12 years earlier.

How to Implement This Strategy

Step 1: Calculate your 8% payment

Use a mortgage calculator to work out what your repayments would be at 8% interest. Write down that weekly or fortnightly amount.

Step 2: Check your mortgage allows extra payments

Most floating and revolving credit facilities allow unlimited extra payments. Fixed-rate mortgages often have limits-typically 5% of the loan balance per year without penalty.

If you're on a fixed rate with limited overpayment allowance, make sure to use the full allowance each year. Any additional savings you want to contribute can go into an offset account or high-interest savings account, then apply it as a lump sum when you refix.

Step 3: Increase payments gradually

If the jump from your current payment to the 8% payment feels too steep, increase gradually. Start by increasing your payments by $50/week for the first three months, then add another $50/week for months four through six, and continue at this pace until you reach the target. This gives your budget time to adjust.

Step 4: Automate the overpayment

Set up an automatic payment for the higher amount. What's automatic gets done. What's optional often doesn't.

When Rates Actually Rise

When your fixed rate expires and you refix at a higher rate, you'll be in one of two positions:

Without this strategy:

"Rates went up, I can barely afford my new payments, I need to cut back on everything."

With this strategy:

"Rates went up, but I've been paying at this level for two years already. Nothing changes for me-except I've already paid down an extra $17,000 in principal."

That's the difference between financial stress and financial confidence.

What If Rates Stay Low?

Some people worry: "What if I pay extra and rates never rise? Wouldn't I be better off investing that money?"

Consider that every extra dollar on your mortgage gives you a guaranteed return of 6-7% (or whatever your rate is) in interest savings-guaranteed and tax-free. A lower mortgage also means reduced risk, with lower required payments if your income ever drops. And once you're ahead on payments, you gain flexibility with options to reduce future payments, access equity, or simply be mortgage-free sooner.

Finding the Extra Money

Where does the extra $100-200/week come from? Here are practical options.

One approach is to capture windfalls by directing any pay rises straight to your mortgage, applying bonuses and tax refunds to principal, and putting unexpected income like gifts or money from sold items toward the loan.

Another strategy involves cutting hidden expenses. Cancelling unused subscriptions can save $50-100/month, reducing dining out frequency could free up another $50-100/month, and making energy efficiency improvements might save $30-50/month on utilities.

You could also increase your income. Renting out a spare room can bring in $150-250/week, while side work or freelancing provides additional earnings. Even selling unused items around your home can contribute meaningful amounts toward your mortgage.

The Psychological Benefit

Beyond the financial maths, there's a psychological benefit to this strategy. Living below your means-even when you could afford more-creates margin in your life.

You're not stressed about rate announcements. You're not worried about whether you can afford your home. You've built a buffer between your income and your essential expenses.

That peace of mind is worth something too.

Future You Will Be Grateful

Your mortgage rate today might be 5%, 6%, or 7%. But if you pay as though it were 8%, you'll be prepared for whatever rates do, save hundreds of thousands in interest, be mortgage-free years earlier, and sleep better at night.

Calculate your 8% payment today. Then set it up. Future you will be grateful.

Need Help With Your Mortgage?

Our expert advisers are here to guide you through every step of your mortgage journey. Get in touch for a free, no-obligation consultation.

Talk to an Adviser