Home Buyer

Buying a home in New Zealand: how lending works, what banks look for, and practical tips to make the process smoother.

Articles in this topic

What Does LVR Mean?

When applying for a mortgage, borrowers frequently encounter the term LVR (Loan-to-Value Ratio). This metric represents what percentage of the property's value is being borrowed.

Debt to Income Ratios: What Are They and How Are They Measured?

DTI restrictions are now a key part of New Zealand's mortgage lending landscape, with rules in effect since 1 July 2024. These aim to manage financial stability and the level of household debt.

What's the Minimum Deposit to Buy a House in NZ?

A comprehensive guide to NZ house deposit requirements in 2026, covering LVR rules, First Home Loans, KiwiSaver withdrawals, gifted deposits, and how much you can actually borrow.

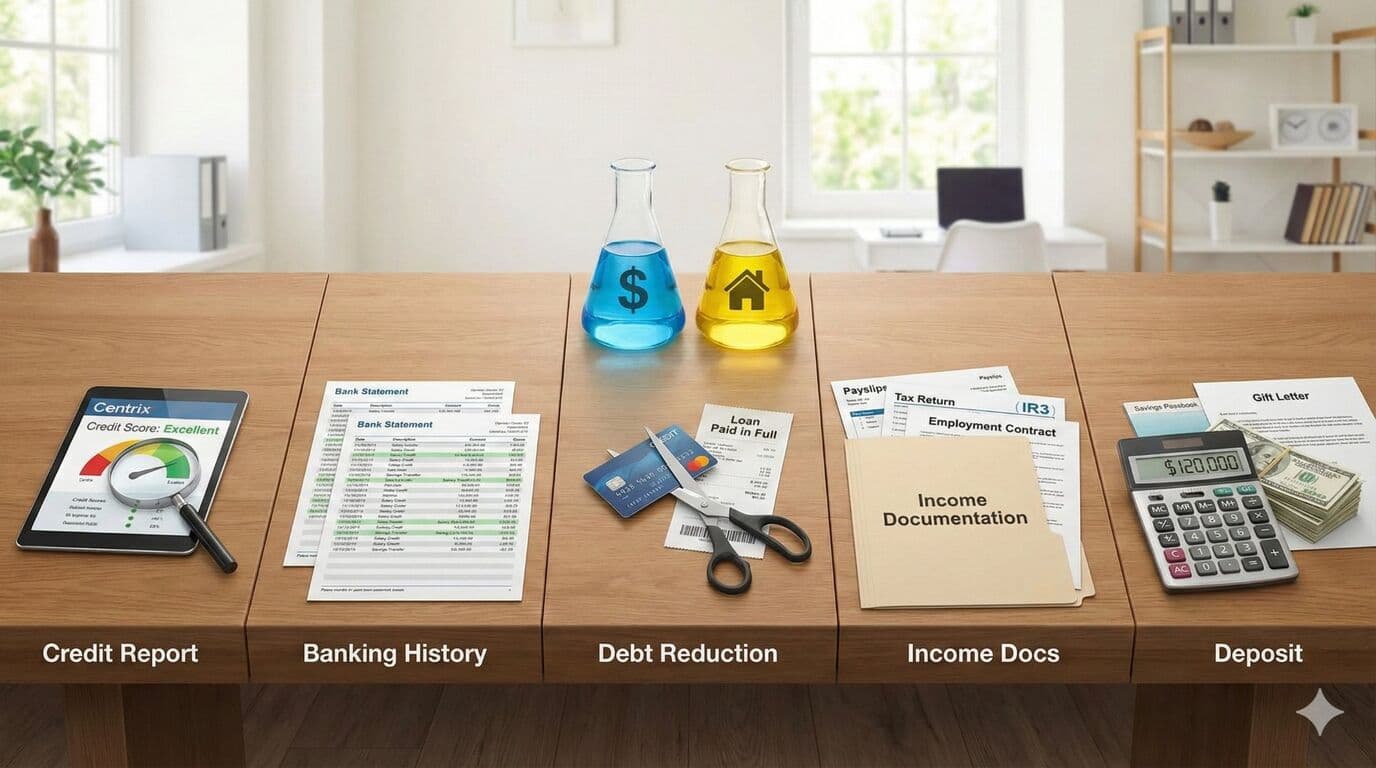

How to Prepare for Your Mortgage Application in New Zealand

Whether you're buying soon or years away, these steps will help you build the strongest possible mortgage application. Start preparing now to maximise your borrowing power.

Downsizing Your Home for Retirement

How selling your family home and moving somewhere smaller can fund your retirement-and whether it is right for you.

New Build vs Existing Home: Which Is Right for You?

Comparing the advantages and disadvantages of building new versus buying an existing property in New Zealand. Make an informed decision for your situation.

How to Choose a Builder for Your New Home

Your choice of builder affects everything from build quality to whether your project finishes on budget. Here is how to find the right one.

Contents Insurance in NZ: Protecting What is Inside Your Home

Contents insurance covers your belongings, but how much do you need and what is actually covered? Here is what to know.

House Insurance in NZ: What Every Homeowner Needs to Know

House insurance protects your biggest asset, but understanding what you are covered for requires looking beyond the premium. Here is what matters.

Downsizing Your Home in Retirement: Financial and Lifestyle Considerations

Selling the family home and moving somewhere smaller is a common retirement strategy. Here is what to consider before making the move.

15 Smart Ways to Increase Your Home's Value and Unlock Equity for Investment

Cost-effective home improvements that can boost property value and unlock equity for investment purposes.

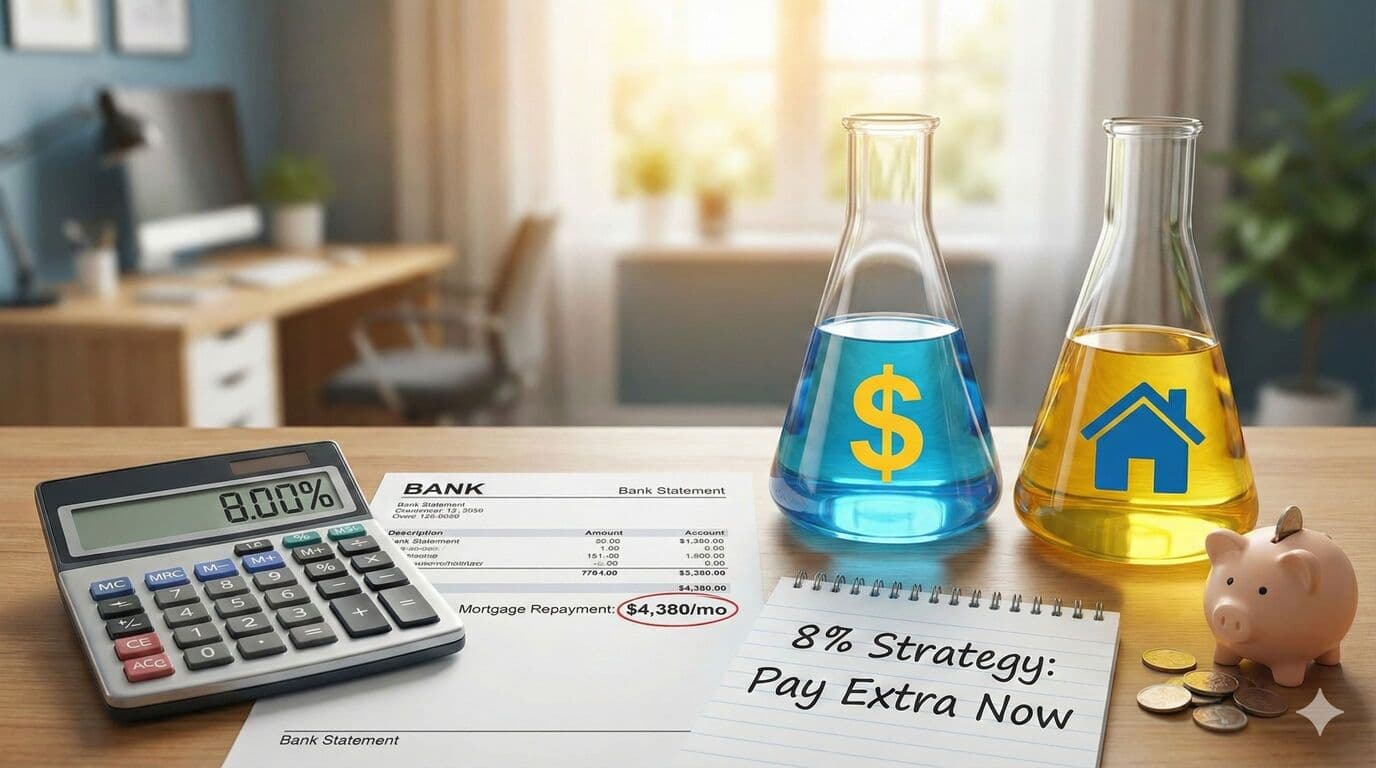

Your Mortgage Rate is 8%

A financial strategy where homeowners should mentally prepare for higher interest rates by adjusting repayments as if their rate were 8%.

When Should You Transfer Your Overseas Savings if You're Buying a Home in NZ?

Timing considerations for expats converting foreign currency into New Zealand dollars before purchasing property.

What Your Mortgage Application and Tinder Profile Have in Common (But Shouldn't)

Both involve presenting yourself favorably, but mortgage lenders require financial honesty rather than curated self-presentation.

What to Check Before Buying a Property in New Zealand

A comprehensive due diligence checklist for New Zealand property buyers, including LIM reports, building inspections, title searches, and costs to budget for.

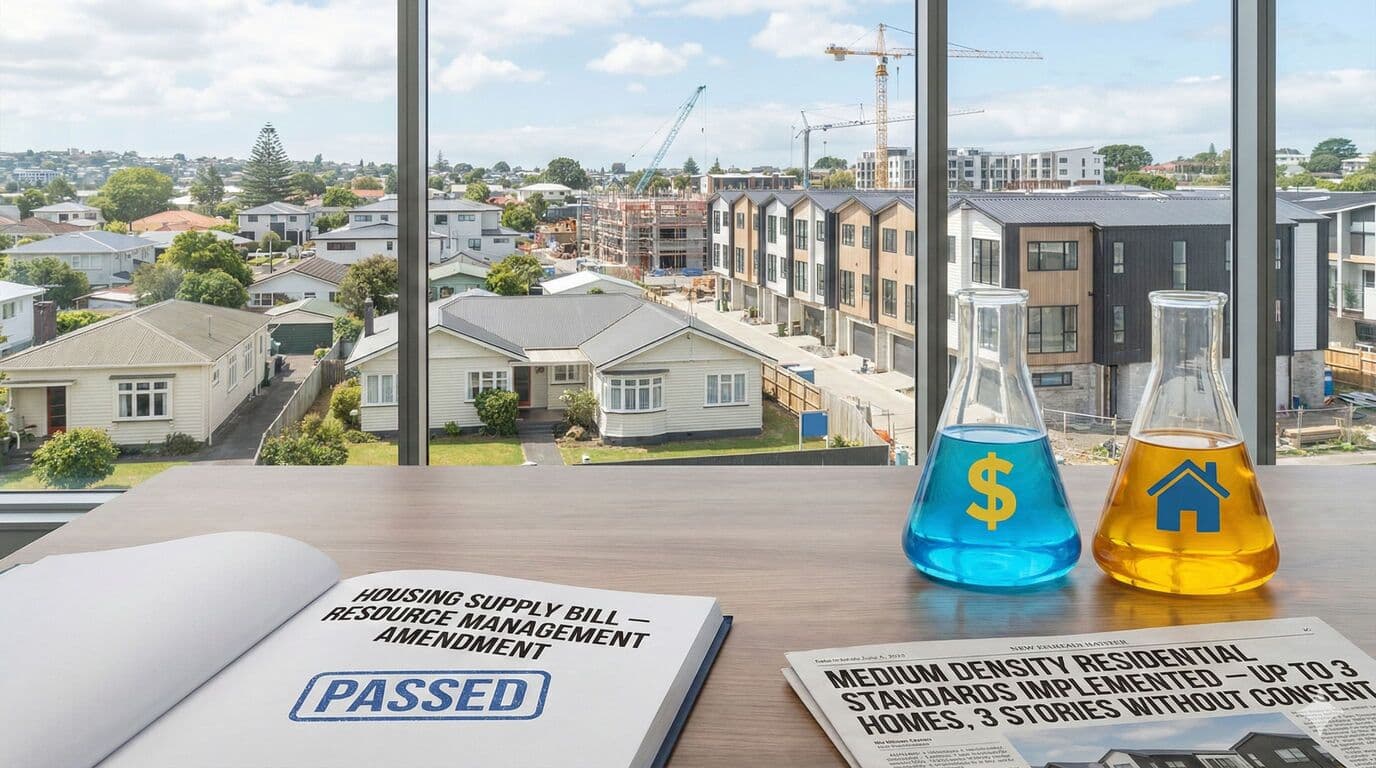

What Was the Housing Supply Act About?

The Resource Management (Enabling Housing Supply) Amendment Act 2021 transformed urban development rules, enabling medium-density housing across major cities.

What Happens When You Go to Buy Your Next House?

A guide addressing the complexities of purchasing a subsequent property after owning a home.

What Happens If Your Registered Valuer's Report Is Too Low?

Banks use official valuation reports-not purchase prices-to determine lending amounts, which can create challenges when valuations fall short.

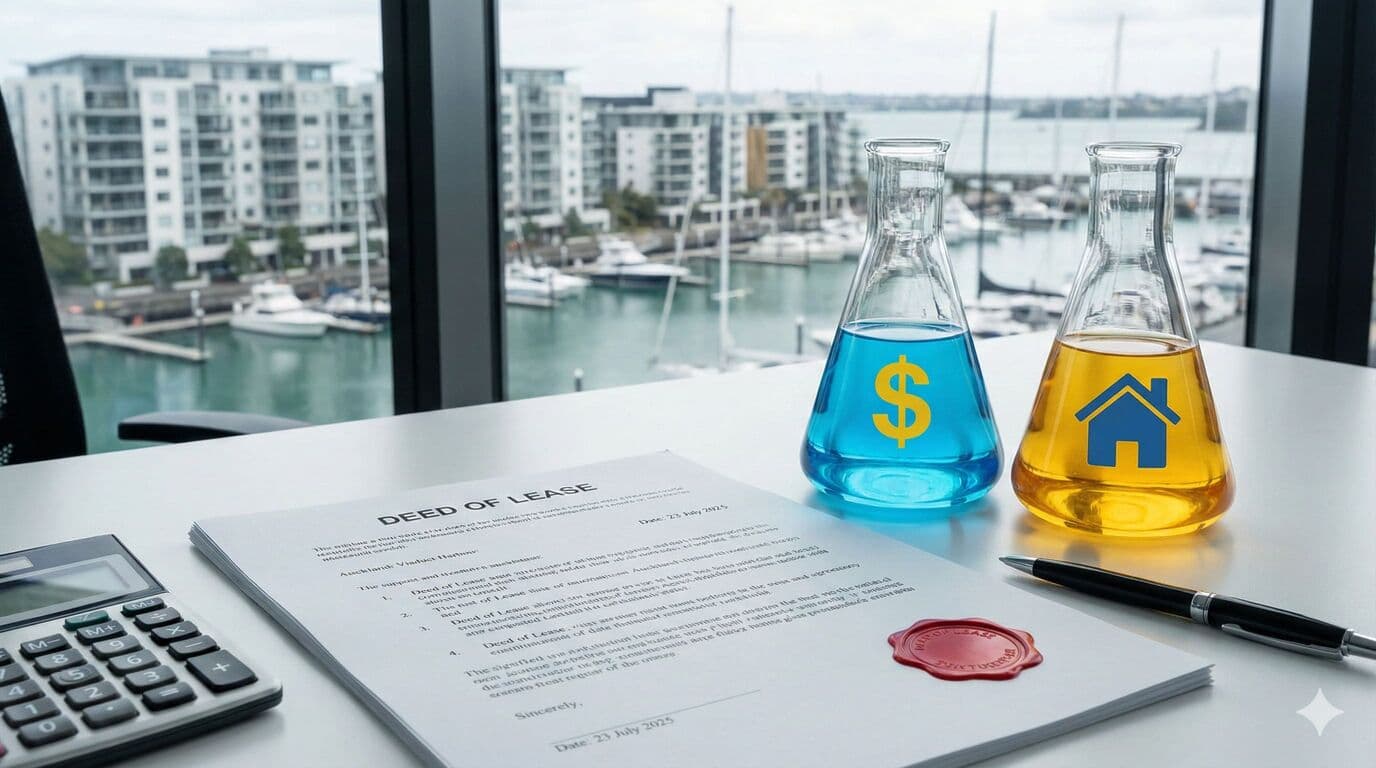

Understanding Leasehold Property Ownership in New Zealand

With leasehold, you purchase the right to occupy land and buildings for a set period rather than owning the land outright.

When Should You Get Your Business Accounts Done for a Mortgage Application?

Self-employed borrowers face distinct challenges when applying for mortgages. Banks require formal financial statements to verify income.

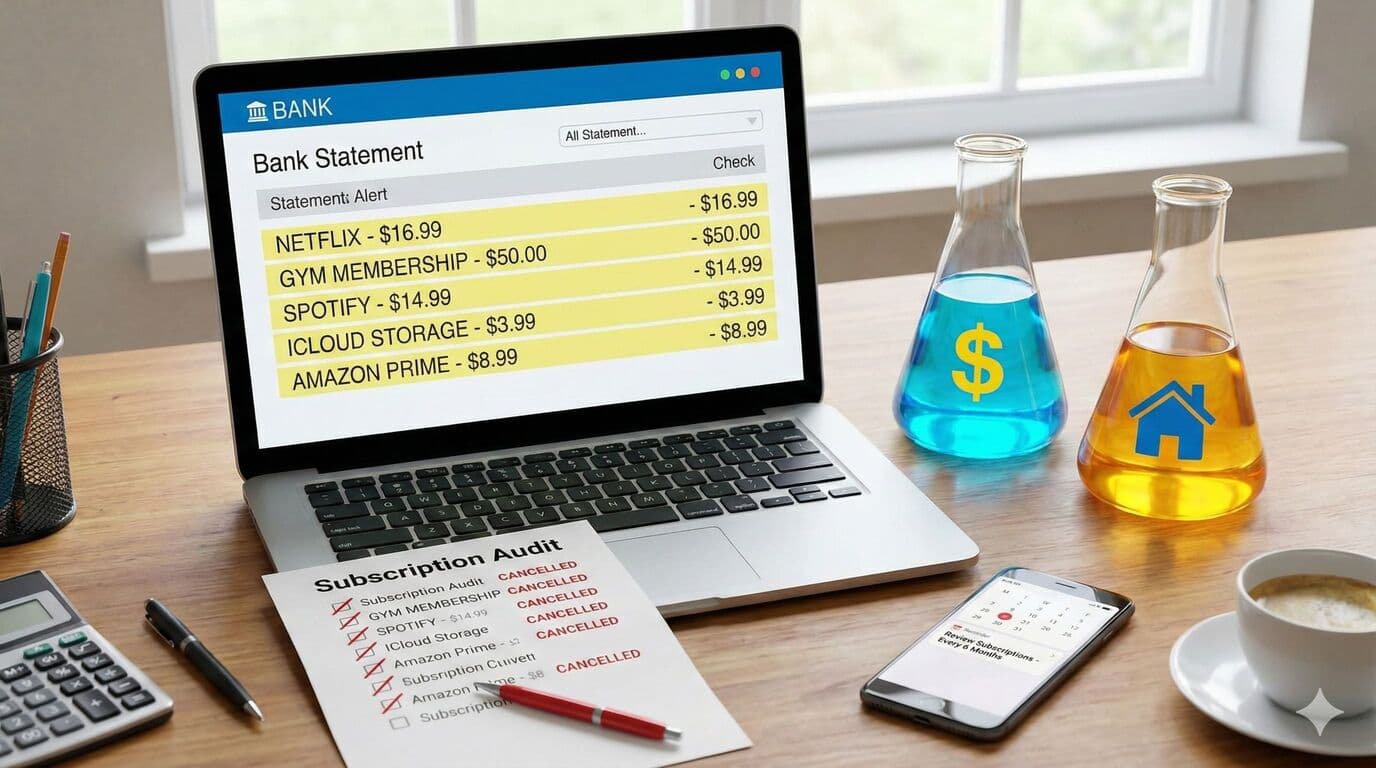

Small Steps: Review Your Direct Debits and Save Money

Many people forget about recurring charges like streaming services and gym memberships that quietly leave accounts each month.

How to Improve Your Credit Report in NZ: Small Steps That Make a Big Difference

Even if your report needs work, you don't have to overhaul your finances overnight. Here's practical guidance for strengthening your credit.

Revolving Credit vs Floating Mortgage Account: What's the Difference?

Two flexible mortgage options available to New Zealand homeowners. Both operate on floating interest rates that fluctuate with market conditions.

Renovate Your Home or Pay Down Your Mortgage?

Should NZ homeowners prioritize home renovations or mortgage reduction? Here are the key considerations.

Property Experts You Need on Your Team When Buying a Home

Essential professionals to assemble when purchasing property in New Zealand.

What Is Price by Negotiation?

When properties are listed as 'Price by Negotiation,' sellers invite offers without setting a fixed asking price. Learn practical negotiation tactics for the NZ property market.

Mortgagee Sales in NZ: Bargain or Big Risk?

When property prices surge and interest rates climb, mortgagee sales resurface. While they appear to offer discounted properties, buyers must understand the risks.

Preparing For Your Mortgage – Documentation

A comprehensive guide for mortgage applicants in New Zealand on required documentation to strengthen your application.

Buying a House with Bitcoin – Can It Be Done in NZ?

While theoretically possible if both parties agree, significant practical barriers exist for buying property with cryptocurrency in New Zealand.

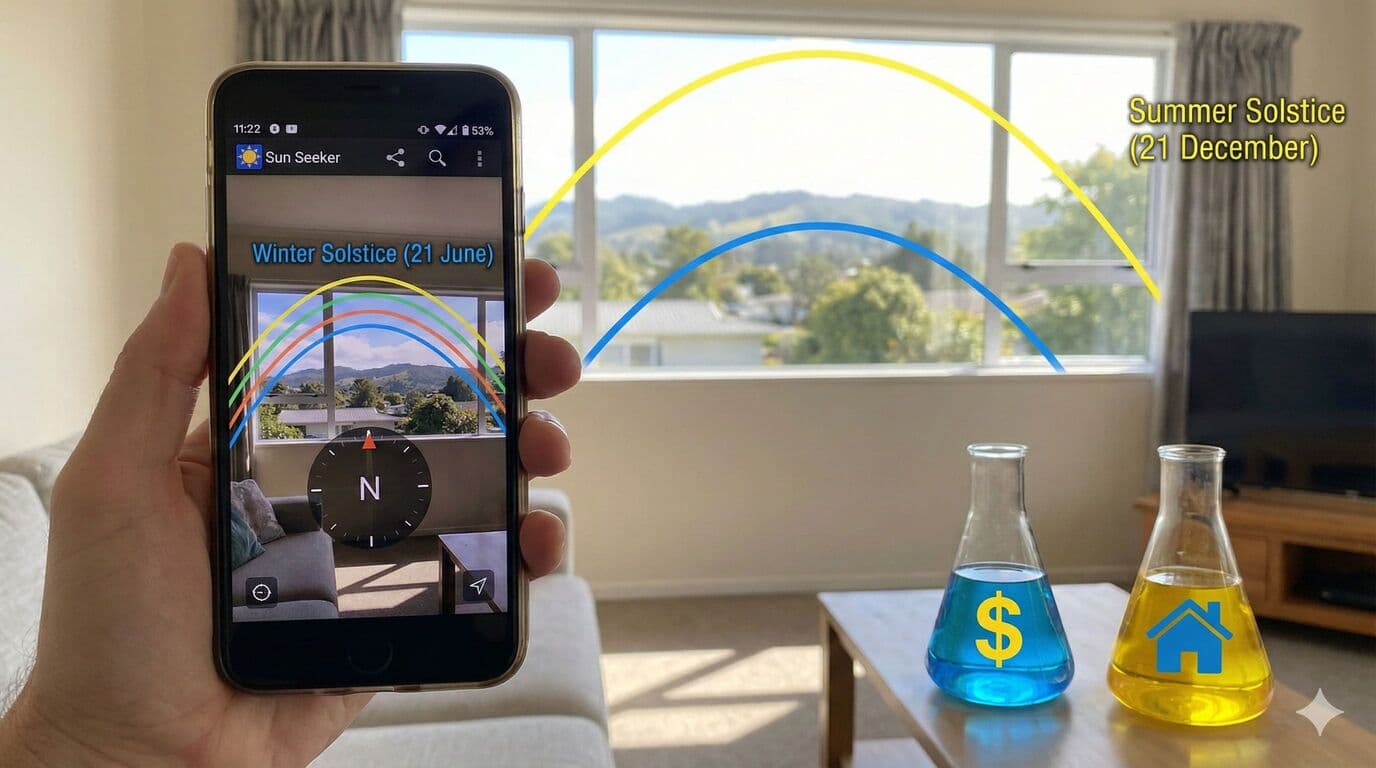

Sun Seeker: The Essential App for Evaluating Property Sun Exposure in NZ

Learn how the Sun Seeker app helps New Zealand property buyers evaluate sun exposure before purchasing. This augmented reality tool shows exactly where sunlight will fall throughout the year.

App of the Month – Gaspy

Gaspy helps New Zealand users locate the cheapest fuel prices nearby. Fuel savings are accessible low-hanging fruit in household budgeting.

Mortgage Calculator: How to Find the Best One

How to choose a mortgage calculator that actually helps you plan, plus recommendations for the best NZ-specific tools including sorted.org.nz and interest.co.nz.

9 Tips for Making a Winning Offer by Tender

Buying a home by tender is one of the more flexible and private ways to purchase property in New Zealand. Here's how to craft a strategic offer.

Is It Worth Getting a Flatmate to Help Pay My Mortgage?

A spare room represents significant untapped earning potential. Here's how a flatmate could accelerate your mortgage repayment.

How to Correctly Export Your Bank Statements

Your mortgage advisor requires bank statements for the application process. Here's how to get the correct formats from major New Zealand banks.

How Much Does a Credit Card Affect Your Lending?

Most people don't realize how significantly credit cards impact mortgage eligibility. Even unused credit limits reduce borrowing capacity.

How Do You Get a Mortgage on a Tiny Home?

Tiny homes present unique financing challenges. Here's what you need to know about securing a mortgage for compact living spaces.

Five Steps You Can Take to Make Your Mortgage Application Easier

Preparation is key to a smooth mortgage application. Here are five practical steps to strengthen your position before applying.

Everything You Need to Know About Debt: Good, Bad, and Grey

Understanding the difference between good debt, bad debt, and grey debt can help you make smarter financial decisions.

The CCCFA: What Property Buyers Need to Know After the 2024 Reforms

The Credit Contracts and Consumer Finance Act (CCCFA) has been significantly reformed since 2024, making mortgage lending more accessible while maintaining responsible lending principles.

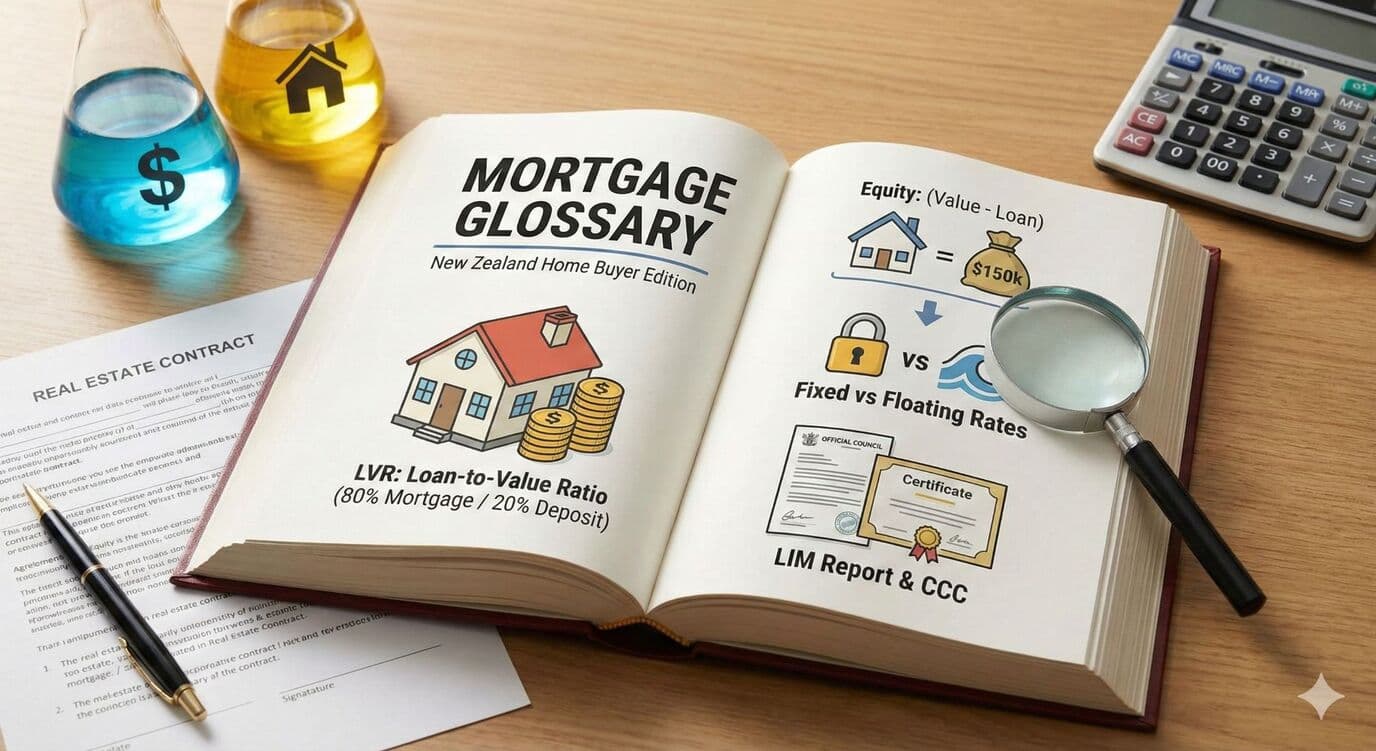

Mortgage Glossary: Common Terms Every Home Buyer Should Know

Buying your first home comes with a flood of new terms-LIM reports, equity, LVRs, CCCs, and more. This comprehensive glossary helps you understand essential mortgage terminology.

All About Conveyancing

This article explores the conveyancing process when purchasing property in New Zealand, featuring insights from a property lawyer.

6 Tips for Bidding at Auction (and How to Prepare Like a Pro)

Buying a home at auction can be both exhilarating and nerve-wracking. With the right preparation and a clear game plan, auctions can be one of the most transparent ways to buy a property.

10 Annual Home Maintenance Tasks Most Homeowners Forget

A practical annual home maintenance checklist to help homeowners keep their properties safe, efficient, and in good condition.

Small Steps: Check Your Credit Score for Free

Most New Zealanders don't think about their credit score until they're applying for a mortgage, car loan or even a mobile phone contract.

Better Budget: Council Rates

Council rates are a significant annual expense for homeowners. Understanding how rates are calculated, when to object, and payment options can help you manage this cost.

Better Budget: Smoke Alarms

Smoke alarms save lives, but many NZ homes have outdated or incorrectly placed alarms. Understanding the current requirements helps ensure your family is protected.

Better Budget: Draught Proofing

Up to 25% of winter heat loss from NZ homes is caused by draughts. Simple DIY draught proofing costs under $50 and can noticeably improve comfort and reduce heating bills.

Better Budget: LED Lighting

LED bulbs use up to 85% less electricity than incandescent or halogen bulbs. Replacing the lights in your home is a low cost improvement with genuine ongoing savings.

Better Budget: Choosing the Right Electricity Plan

The average New Zealand household can save $350 per year by switching electricity plans. Understanding low user versus standard plans and time of use pricing can significantly reduce your power bills.

Better Budget: Hot Water Cylinders

Hot water typically accounts for 30% of household energy costs. Understanding temperature settings, insulation, and when to upgrade can save hundreds annually.

Better Budget – All About Your Heat Pump

Heat pumps represent an efficient heating solution. According to GenLess, "a heat pump is the most energy-efficient way of using electricity to heat your home."

Buying a Better Home in a Hot Property Market

If you're fortunate enough to have owned a house for a couple of years, property appreciation has likely increased your wealth. Should you use your increased equity to upgrade?

How to Move Cities When You Have a Mortgage

With remote work becoming increasingly common, relocating to smaller, more affordable cities is now viable for many professionals.

What Does $1,000,000 Buy You in the Major NZ Cities?

What does one million dollars actually buy you in New Zealand? The answer varies dramatically depending on location-from below-median in Auckland to multiple investment properties in Dunedin.

How Expat Kiwis Can Buy Property in NZ and Return Home

Many Kiwis living overseas are considering returning home and buying property. Here is what expat New Zealanders need to know about getting a mortgage remotely.

Stop Looking at the Performance of House Prices

Almost every potential house buyer will ask "what are house prices doing at the moment?" This concern stems from not wanting to purchase a property today only to watch its value decline.

What Is an Easement? Understanding Property Rights in New Zealand

Easements are a legal but often overlooked element of property ownership in New Zealand. If you're buying a property-especially a new build-it's highly likely your title includes an easement.

Case Study: When You Are Just Short of 20% Deposit

This case study examines what happens when your deposit falls just short of the 20% threshold-and how a small shortfall can cost thousands in fees.

The Real Cost of Credit Cards on Your Mortgage Capacity

Credit cards are a familiar fixture in most New Zealand wallets. But when it comes time to apply for a mortgage, those little pieces of plastic could be reducing your borrowing power more than you realise.

New Build vs Existing Home: Which Should You Buy?

For many Kiwis, one of the first big questions in the home-buying journey is whether to purchase a brand-new home or an existing one.

Can I Get a Top-Up on My Mortgage?

A mortgage top-up is an additional loan added to your existing home loan. The bank increases the amount owed on your mortgage and releases the difference as cash.

How Soon Can You Reapply for a Mortgage After Being Declined?

Being turned down for a mortgage can be gutting-especially when you've started picturing life in a new home. But this one can be remedied.

Can I Buy a Home With Friends? What You Need to Know About Co-Ownership

Can New Zealand first home buyers purchase property together with friends? Here are the practical and legal considerations.

What Happens When You Buy a House in New Zealand?

Buying a house for the first time isn't just a financial step-it's an emotional rollercoaster. Here's your spoiler-free guide to the full home buying journey.

How to Get a Mortgage in New Zealand: The 7-Step Process for First Home Buyers

The mortgage process intimidates many first-time home buyers, but it follows a structured pathway. Here's what to expect through seven key stages.

How Offset Mortgages Work in New Zealand

An offset mortgage links everyday bank accounts to your home loan. Rather than earning interest on savings, the money in those accounts is treated as if it's reducing the mortgage balance.

How Does a Prenup Affect Your Application for a Mortgage?

For many couples, buying a home together represents one of the biggest financial steps they'll ever take. Before signing mortgage papers, one legal document can be as important as your home loan: a prenup.

Mortgage Strategies for Self-Employed and Gig Economy Workers

If you're self-employed or working in the gig economy, you've probably noticed that applying for a mortgage isn't quite as straightforward as it is for salaried employees.

What Is a Revolving Credit Account and Should You Use One?

A revolving credit account is a flexible home loan structure functioning similarly to a large overdraft. Rather than having an entire mortgage on a fixed schedule, a portion operates as a revolving facility.

When Do You Need a Registered Valuer's Report When Purchasing a House?

If you're buying a home or applying for finance, you may be asked for a Registered Valuer's Report. This isn't just another online estimate or a council rating figure.

5 Things To Know About Your Mortgage Pre-Approval Letter of Offer

Good news! You're pre-approved for your mortgage! Here are the most important parts of the letter of offer you'll receive.

Purchasing at Auction – A Step by Step Guide

Buying at auction can be exciting but also intimidating. Here's your complete guide to navigating the auction process with confidence.

Budgeting with PocketSmith: A Complete Guide for NZ Home Buyers

PocketSmith is New Zealand's homegrown budgeting app that helps home buyers track expenses and prepare for mortgage applications. Learn how this Kiwi-made software can transform your financial planning.

Top 5 Most Useful Property Websites in New Zealand

Whether you're buying your first home or comparing council rates across districts, here are the top five property websites that are genuinely helpful.

What Is a Priority Amount in a Mortgage?

If you've reviewed your property's title after securing a home loan, you may have spotted something unexpected-a much higher figure than the amount you actually borrowed.

What Counts as Genuine Savings When Applying for a Mortgage?

When applying for a mortgage in New Zealand, not all deposit money is treated equally. That's where the term 'genuine savings' comes in.

2 Bank Account Tips The Banks Will Never Tell You

Banks operate as profit-focused businesses with reputations that don't always reflect reality. Here are two recommendations that banks typically won't share.

Frequently asked questions

What is LVR and how is it calculated?

LVR (Loan-to-Value Ratio) is calculated by dividing your loan amount by the property value. For example, a $600,000 mortgage on an $800,000 property equals 75% LVR.

What LVR do I need to buy a house in NZ?

For owner-occupied homes, banks may lend above 80% LVR for up to 25% of their new owner-occupier lending. For investment properties, banks may lend above 70% LVR for up to 10% of their new investor lending. This means having a deposit that keeps you below these high-LVR thresholds (e.g., 20% for owner-occupier, 30% for investor) generally gives you more options.

Are there any exemptions to LVR rules?

Yes, several types of lending are typically exempt from LVR restrictions. These include Kāinga Ora loans (including First Home Loans), same/lower-value refinancing, portability with no increase, bridging finance, non-routine remediation, construction loans, and some newly built homes bought from the developer within 6 months of completion.

Why do banks have LVR restrictions?

The Reserve Bank implemented LVR controls in 2013 to moderate rapid house price increases and reduce financial system risk. By restricting borrowing relative to property value, the policy encourages caution among buyers without raising interest rates across the board.

How does LVR affect my interest rate?

Higher LVR loans (above 80% for owner-occupiers, or above 70% for investors) are considered riskier by banks, which may result in slightly higher interest rates or additional fees. Lower LVR positions typically give you access to better rates and more lending options.

What is the difference between LVR for investors and owner-occupiers?

For owner-occupiers, high-LVR lending is considered above 80% LVR, with banks able to allocate up to 25% of new owner-occupier lending in this category. For investors, high-LVR lending is above 70% LVR, with banks able to allocate up to 10% of new investor lending in this category.

How can I improve my LVR position?

You can improve your LVR by saving a larger deposit, paying down your existing mortgage faster, or benefiting from property value increases. Using [genuine savings](/blog/what-counts-as-genuine-savings-when-applying-for-a-mortgage) over time demonstrates financial responsibility to lenders.

Does LVR affect my ability to access equity?

Yes, your LVR determines how much equity you can access for renovations, investment property deposits, or other purposes. Most banks will only lend up to 80% of your property value (or 70% for investors), so your usable equity is the difference between this threshold and your current LVR.