Buying your first home is one of the biggest financial decisions you'll ever make. The good news is that you don't have to wait until you're ready to buy to start preparing. Taking action today can significantly strengthen your lending prospects and make the application process smoother when you're ready to take the plunge.

1. Obtain Your Credit Report

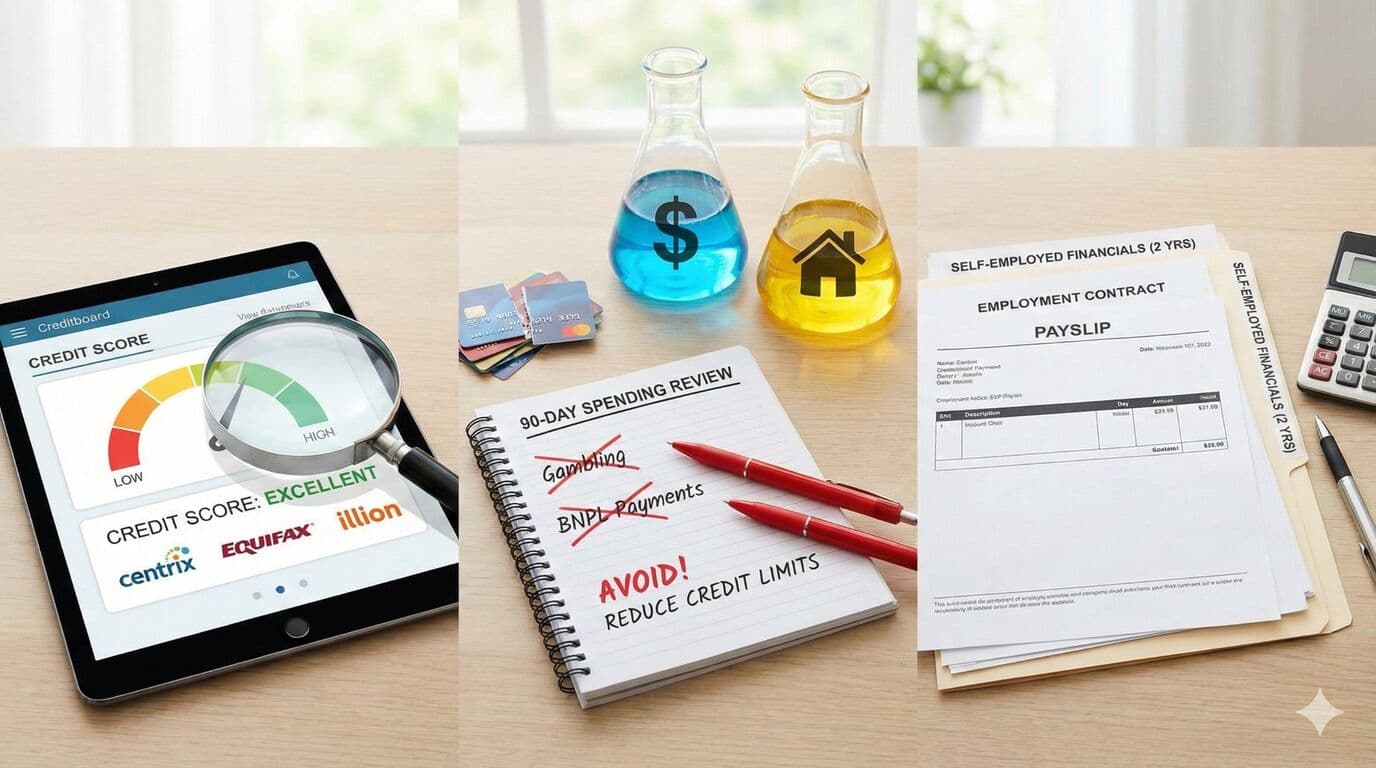

Review your credit history before lenders do. In New Zealand, you can check your credit report for free through Centrix, Equifax, or illion. Small hiccups-like a missed payment, an old default, or even an error on your file-can affect how a lender views your application.

Early identification of problems allows time for corrections before formal submission. If you find errors, contact the credit bureau to have them investigated and corrected. If you have legitimate defaults, focus on paying them off and building positive payment history over the coming months.

2. Organize Your Spending Patterns

Banks examine the previous 90 days of transactions to assess financial discipline. What they're looking for is evidence that you can manage money responsibly-not that you live like a monk.

Red flags include gambling transactions, frequent Buy Now Pay Later purchases, and inconsistent spending patterns. Establish a dedicated account for regular expenses with automatic payments to demonstrate responsible money management. Avoid large unexplained cash withdrawals and keep discretionary spending reasonable.

One thing many first-home buyers don't realise: credit cards significantly impact your borrowing capacity. Banks apply a 3-5% repayment rate to your total credit limit-not your balance. Every $10,000 in credit card limits can reduce your borrowing capacity by $50,000-60,000. Consider reducing or closing unused cards before applying.

3. Prepare Income Documentation

Lenders require recent payslips to verify income stability and composition. For PAYE employees, gather your three most recent payslips plus any evidence of bonuses or commission. If you receive variable income, having 6-12 months of payslips helps demonstrate consistency.

Self-employed applicants need accountant-prepared financial statements-typically two years of accounts plus tax returns. Contractors should have their current contract terms, recent invoices, and ideally an accountant's letter confirming income.

Gathering these proactively prevents delays during the application timeline. A complete application typically takes 3-5 working days for pre-approval, but drip-feeding documents can extend this significantly.

Understanding Your Borrowing Capacity

Before you start house hunting, it's worth understanding how much you can actually borrow. Banks currently stress-test your affordability at around 8%, even though current rates may be lower. This ensures you can handle potential rate increases.

If you're considering the First Home Loan through Kāinga Ora, check eligibility early. You'll need to meet the First Home Loan criteria, including the current income caps, a minimum 5% deposit, buying a home to live in as your primary residence, and the lending criteria of a participating lender.

KiwiSaver Preparation

If you're planning to use your KiwiSaver for your deposit, confirm your eligibility now. You must have been a KiwiSaver member for at least three years, and at least $1,000 must remain in your account after withdrawal. Contact your provider to get a withdrawal eligibility letter-you'll need this for your mortgage application.

Start Today, Thank Yourself Later

The more prepared you are before applying, the smoother your journey to homeownership will be. Start these steps today, even if you're 6-12 months away from buying. Your future self will thank you.

Need Help With Your Mortgage?

Our expert advisers are here to guide you through every step of your mortgage journey. Get in touch for a free, no-obligation consultation.

Talk to an Adviser