अपना पहला घर खरीदना सबसे बड़े financial decisions में से एक है जो आप कभी करेंगे। अच्छी बात यह है कि आपको तैयारी शुरू करने के लिए खरीदने के लिए तैयार होने तक इंतजार नहीं करना है। आज action लेना आपके lending prospects को काफी मजबूत कर सकता है और application process को आसान बना सकता है जब आप तैयार हों।

1. अपनी Credit Report लें

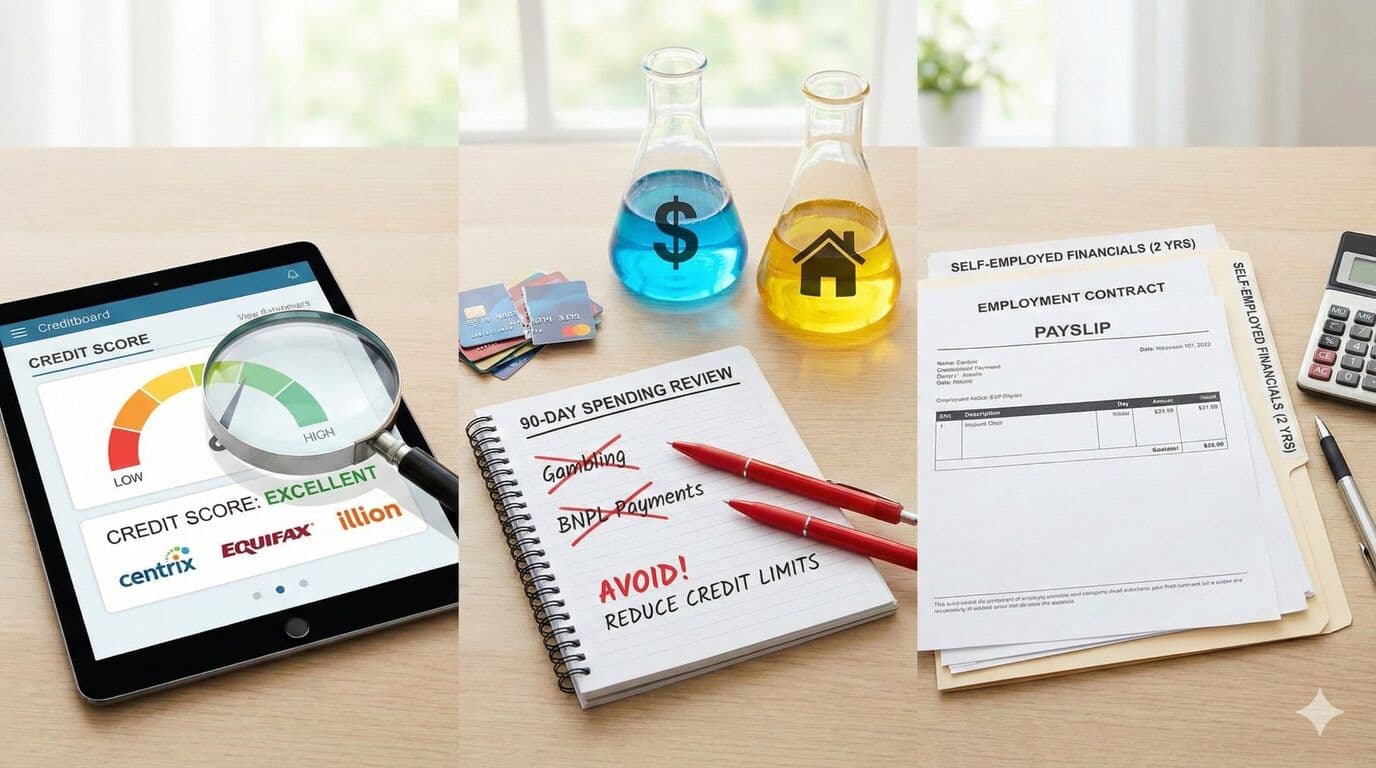

Lenders से पहले अपनी credit history review करें। New Zealand में, आप Centrix, Equifax, या illion के through free credit report check कर सकते हैं। छोटी गलतियां, जैसे missed payment, पुराना default, या अपनी file पर error, affect कर सकती हैं कि lender आपकी application को कैसे देखता है।

Problems की जल्दी पहचान करने से formal submission से पहले corrections का समय मिलता है। अगर आपको errors मिलें, तो credit bureau से contact करें और उन्हें investigate और correct करवाएं। अगर आपके legitimate defaults हैं, तो उन्हें pay off करने और आने वाले months में positive payment history build करने पर focus करें।

2. अपने Spending Patterns Organize करें

Banks financial discipline assess करने के लिए पिछले 90 days के transactions examine करती हैं। वे देखना चाहती हैं कि आप responsibly money manage कर सकते हैं, यह नहीं कि आप monk की तरह रहते हैं।

Red flags में gambling transactions, frequent Buy Now Pay Later purchases, और inconsistent spending patterns शामिल हैं। Responsible money management demonstrate करने के लिए regular expenses के लिए dedicated account establish करें automatic payments के साथ। Large unexplained cash withdrawals से बचें और discretionary spending reasonable रखें।

एक बात जो बहुत से first-home buyers नहीं जानते: credit cards borrowing capacity को significantly impact करती हैं। Banks आपकी total credit limit पर 3-5% repayment rate apply करती हैं, आपके balance पर नहीं। हर $10,000 credit card limits में आपकी borrowing capacity $50,000-60,000 कम कर सकती है। Apply करने से पहले unused cards reduce या close करने पर विचार करें।

3. Income Documentation तैयार करें

Lenders income stability और composition verify करने के लिए recent payslips require करते हैं। PAYE employees के लिए, अपनी तीन most recent payslips plus bonuses या commission का evidence gather करें। अगर आपको variable income मिलती है, तो 6-12 months के payslips रखना consistency demonstrate करने में help करता है।

Self-employed applicants को accountant-prepared financial statements चाहिए, typically दो साल के accounts plus tax returns। Contractors के पास अपने current contract terms, recent invoices, और ideally accountant's letter confirming income होनी चाहिए।

ये proactively gather करना application timeline के दौरान delays prevent करता है। Complete application typically pre-approval के लिए 3-5 working days लेती है, लेकिन drip-feeding documents इसे significantly extend कर सकती है।

अपनी Borrowing Capacity समझना

House hunting शुरू करने से पहले, यह समझना worth है कि आप actually कितना borrow कर सकते हैं। Banks currently आपकी affordability को around 8% पर stress-test करती हैं, भले ही current rates lower हों। यह ensure करता है कि आप potential rate increases handle कर सकें।

अगर आप Kāinga Ora के through First Home Loan consider कर रहे हैं, तो जल्दी eligibility check करें। आपको First Home Loan criteria पूरा करना होगा, जिसमें current income caps, minimum 5% deposit, ऐसा घर खरीदना जिसे आप अपनी primary residence के रूप में रहेंगे, और participating lender के lending criteria शामिल हैं।

KiwiSaver Preparation

अगर आप अपने deposit के लिए KiwiSaver use करने की planning कर रहे हैं, तो अभी अपनी eligibility confirm करें। आपको कम से कम तीन साल के लिए KiwiSaver member होना चाहिए, और withdrawal के बाद कम से कम $1,000 आपके account में रहना चाहिए। Withdrawal eligibility letter के लिए अपने provider से contact करें, आपको यह अपनी mortgage application के लिए चाहिए।

आज शुरू करें, बाद में खुद को Thank करें

Apply करने से पहले जितना ज्यादा prepared रहेंगे, homeownership का journey उतना ही smoother होगा। आज ही ये steps शुरू करें, भले ही buying से 6-12 months दूर हों। आपका future self आपको thank करेगा।

Need Help With Your Mortgage?

Our expert advisers are here to guide you through every step of your mortgage journey. Get in touch for a free, no-obligation consultation.

Talk to an Adviser